Growth and Trends in the Global Cell Therapy Manufacturing Market (2024-2034)

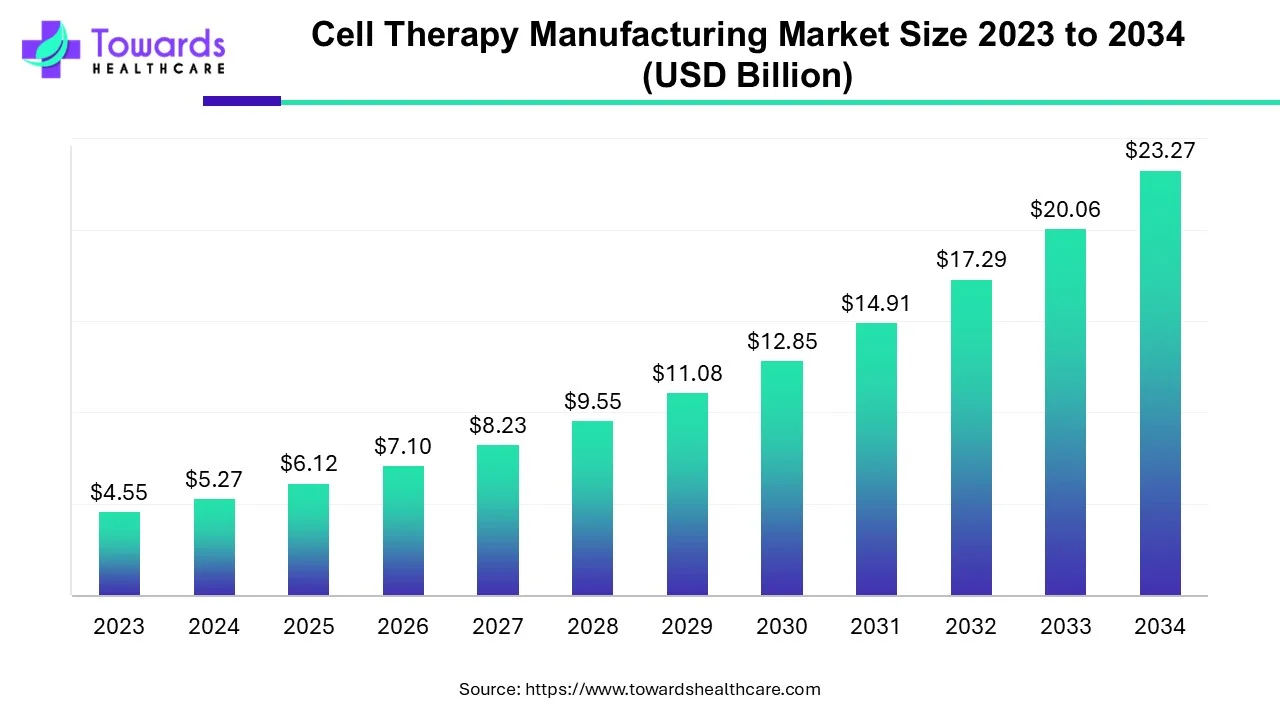

The global cell therapy manufacturing market is projected to grow from USD 5.27 billion in 2024 to USD 23.27 billion by 2034, expanding at a compound annual growth rate (CAGR) of 16% between 2025 and 2034. This growth is being driven by several key factors, including the rising prevalence of chronic diseases, increasing demand for regenerative medicine, and continuous advancements in technology.

Download statistics of this report @ https://www.towardshealthcare.com/download-statistics/5050

Cell therapy manufacturing is the process of producing therapeutic cells to treat various medical conditions. This process involves the extraction, expansion, modification, and quality assurance of cells to generate a sufficient quantity of functional cells. The therapeutic cells can be sourced from the patient’s own body (autologous cells) or from a donor (allogeneic cells). Cell therapies have attracted significant attention due to their potential in treating a wide variety of conditions, such as cancer, cardiovascular diseases, neurodegenerative disorders, and autoimmune diseases.

The increasing need for personalized medicine, advancements in research and development, and the rising number of chronic disease cases are major driving forces in the cell therapy manufacturing sector. Cell therapies offer highly targeted, individualized treatment options that can improve patient outcomes. Additionally, the growing investments in regenerative medicine and supportive regulatory environments are contributing to the market’s expansion. Notably, nearly 90% of cancer cases involve treatments that rely on cell therapies, especially for treating solid tumors.

Segment Insights in the Cell Therapy Manufacturing Market

Autologous Cell Therapy Dominates the Market

In 2024, the autologous cell therapy segment held the largest share of the cell therapy manufacturing market. Autologous cell therapy involves collecting cells from the patient, processing them outside the body, and then reintroducing them into the same patient. This method reduces the risk of immune rejection, leading to better outcomes and fewer side effects, which improves the chances of long-term recovery. The limited availability of immediate donors also makes autologous cell therapy a more viable option.

Allogeneic Cell Therapy: The Fastest-Growing Segment

The allogeneic cell therapy segment is projected to grow the fastest during the forecast period. This type of therapy uses stem cells from healthy donors rather than from the patient’s own body. A major advantage of allogeneic cell therapy is that it bypasses co-morbidities associated with the patient’s disease. The growing number of stem cell banks and improvements in storage technology are fueling this segment’s rapid expansion.

Somatic Cell Technology Leads the Market

In 2024, the somatic cell technology segment was the leader in the global cell therapy manufacturing market. Somatic cell nuclear transfer (SCNT) is a technique that creates viable embryos using body cells and egg cells. It is used to obtain pluripotent cells from cloned embryos or to generate tissues and organs for specific patients. As research and technology continue to advance, this segment’s growth is accelerating.

3D Technology: The Fastest-Growing Technology

The 3D technology segment is expected to experience the highest growth rate during the forecast period. 3D printing is an emerging technology that’s revolutionizing the production of biological products, including cell therapies. This technology enables faster, more accurate, and cost-effective cell therapy manufacturing, creating personalized, cell-laden structures that mimic the complex functions and architecture of native tissues.

Induced Pluripotent Stem Cells Lead in Source

Induced pluripotent stem cells (iPSCs) dominated the market in 2024. iPSCs are cells derived from somatic cells that can develop into any type of cell in the body, making them ideal for applications like disease modeling, drug screening, and developing cell therapies. Their ability to multiply indefinitely and generate various cell types has led to growing demand in the market.

Bone Marrow Segment to See Significant Growth

The bone marrow segment is anticipated to experience strong growth over the forecast period. Stem cells taken from bone marrow can differentiate into red blood cells, white blood cells, or platelets, making them critical for treating blood disorders. The increasing incidence of hematological diseases is driving growth in this segment.

Oncology Leads in Application

The oncology segment held the largest share of the market in 2024. This is due to the rising prevalence of cancer, greater investments in cancer research, and supportive regulatory frameworks. The U.S. FDA has approved several cell and gene therapy products for cancer treatment, further fueling market growth.

Neurological Disorders: The Fastest-Growing Application

The neurological segment is expected to expand rapidly in the coming years. The growing number of neurological disorders, coupled with their complexity, highlights the need for innovative therapies like cell therapy. An aging population and new cell therapy treatments, such as the FDA-approved product for Alzheimer’s disease in 2023, are driving this growth.

Regional Insights: North America Takes the Lead

North America, particularly the United States, dominates the global cell therapy manufacturing market. The region benefits from advanced healthcare infrastructure, a strong regulatory framework, and the presence of key industry players. The U.S. has been a leader in cell therapy research and development, drawing significant investments and fostering collaborations between academia, research institutions, and industry players.

Europe: A Strong Contender in the Market

Europe is another key region for cell therapy manufacturing. Countries like Germany, the United Kingdom, and France have established healthcare systems and regulatory frameworks that support the development and commercialization of cell therapies. The European Medicines Agency (EMA) plays a significant role in ensuring the safety and efficacy of these therapies, while collaborations between academic institutions, hospitals, and industry players continue to drive advancements in the field.

Cell Therapy Manufacturing Market Companies

- Merck KGaA

- Thermo Fisher Scientific

- Catalent, Inc

- Bio-Techne

- Cytiva

- Lonza

- The Discovery Labs

- Novartis AG

- Bristol-Myers Squibb Company

- Gilead Sciences, Inc.

Our Table of Content (TOC) covers key healthcare market segments, materials, technologies and trends—helping you navigate market shifts and make informed decisions: https://www.towardshealthcare.com/table-of-content/cell-therapy-manufacturing-market

Access exclusive insight now @ https://www.towardshealthcare.com/price/5050

We’ve prepared a service to support you. Please feel free to contact us at sales@towardshealthcare.com

Web: https://www.towardshealthcare.com

Visit Dental Specifics: https://www.towardsdental.com

Get the latest insights on industry segmentation with our Annual Membership: Get a Subscription

For Latest Update Follow Us: https://www.linkedin.com/company/towards-healthcare